카드 1 / 8

Korean Energy Drink in the US: Where to Compete Against Monster ($35% share), Red Bull (32%), and Celsius (10%) (2026)

TL;DR

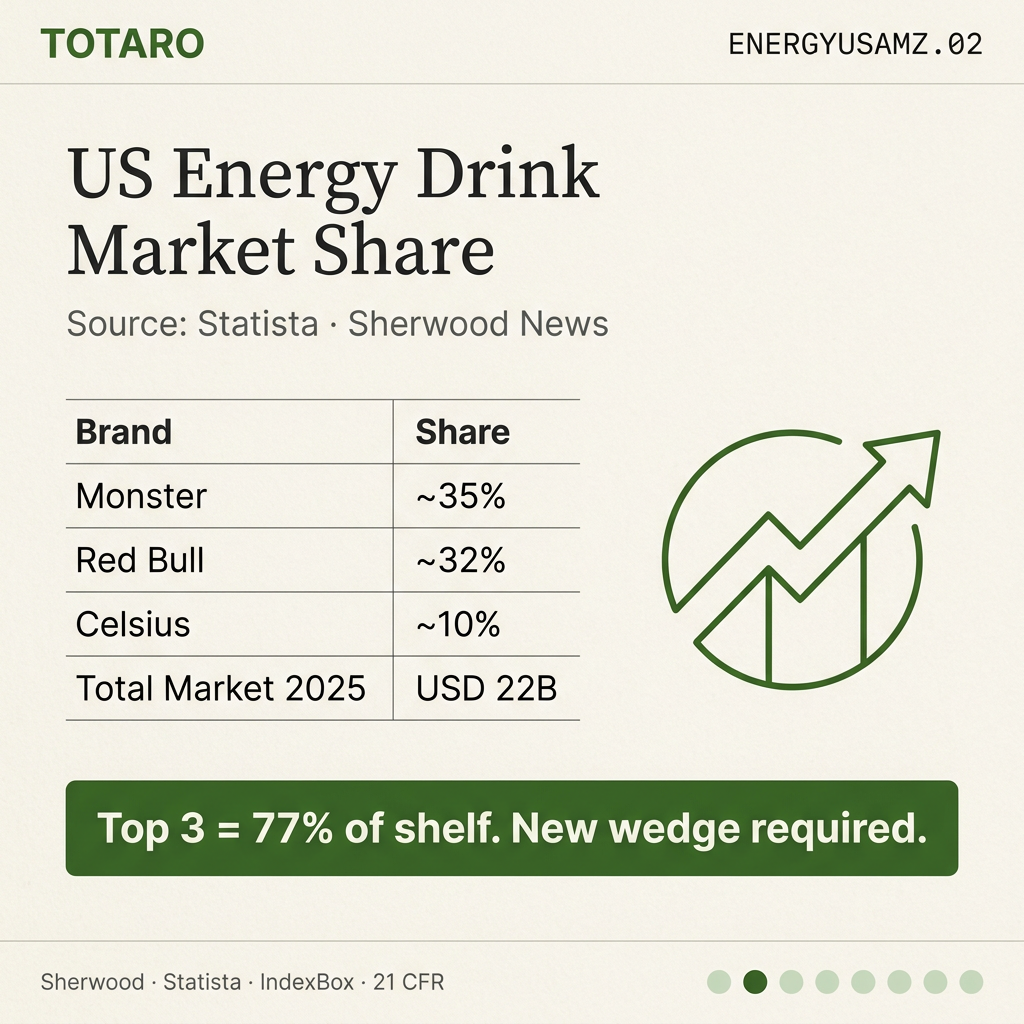

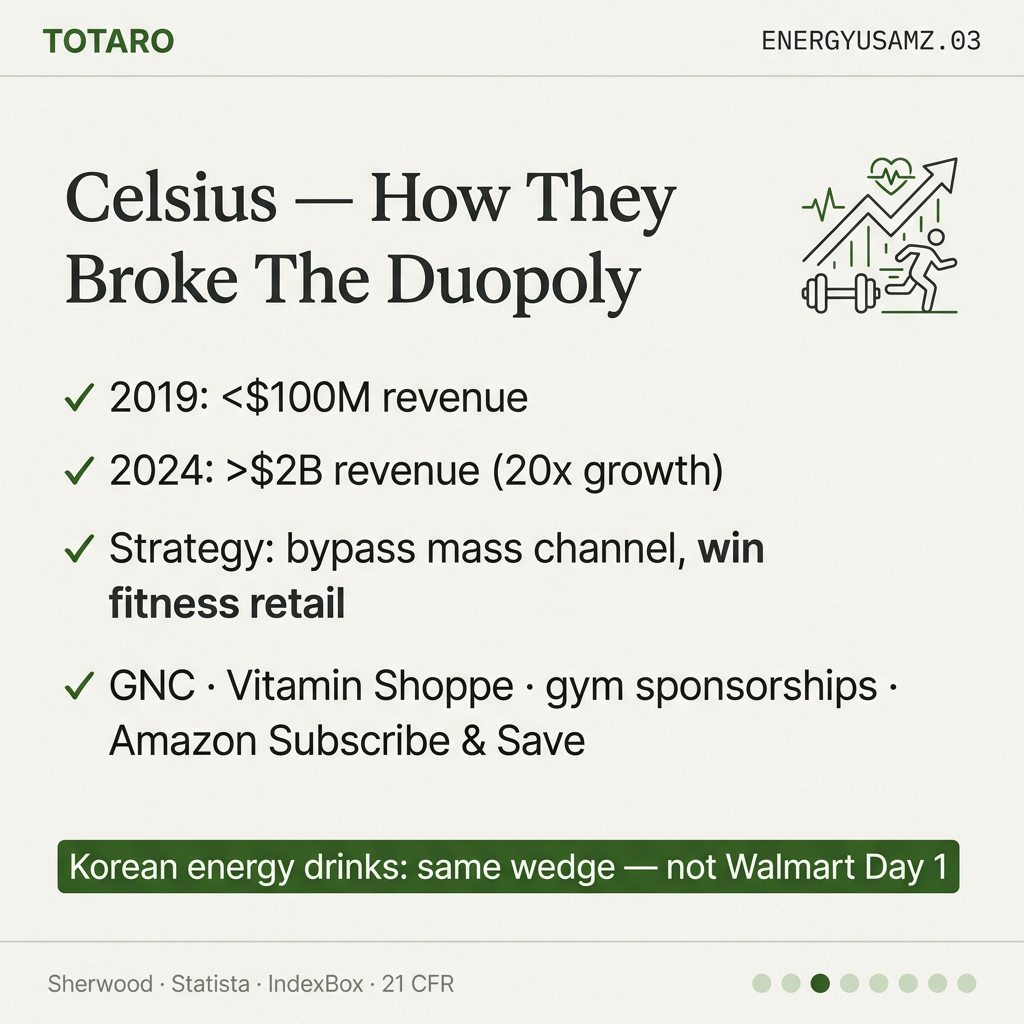

US energy drink market is approximately USD 22 billion in 2025 (Sherwood News — Energy Drink Sales). The top 3 control about 77% of the shelf: Monster ~35%, Red Bull ~32%, Celsius ~10% (Accio — Top Energy Drink Brands 2026). Celsius grew from <$100M in 2019 to >$2B in 2024 (IndexBox — Celsius Holdings). Korean energy drinks need a non-mass-shelf entry path — fitness retail, Amazon DTC, and Asian-grocery chains — before any pitch to mass chains.

1. The Celsius Lesson

Celsius proved a new player could break Monster/Red Bull duopoly within 5 years — by bypassing the convenience-store/mass channel initially and winning fitness retail (GNC, Vitamin Shoppe), gym sponsorships, and Amazon Subscribe & Save. Korean energy drinks (Lotte HOT6, Burn Korean energy, BAEKSESJU energy) need a similar wedge: not Walmart day-one, but a positioned channel.

2. Where Korean Energy Drinks Win

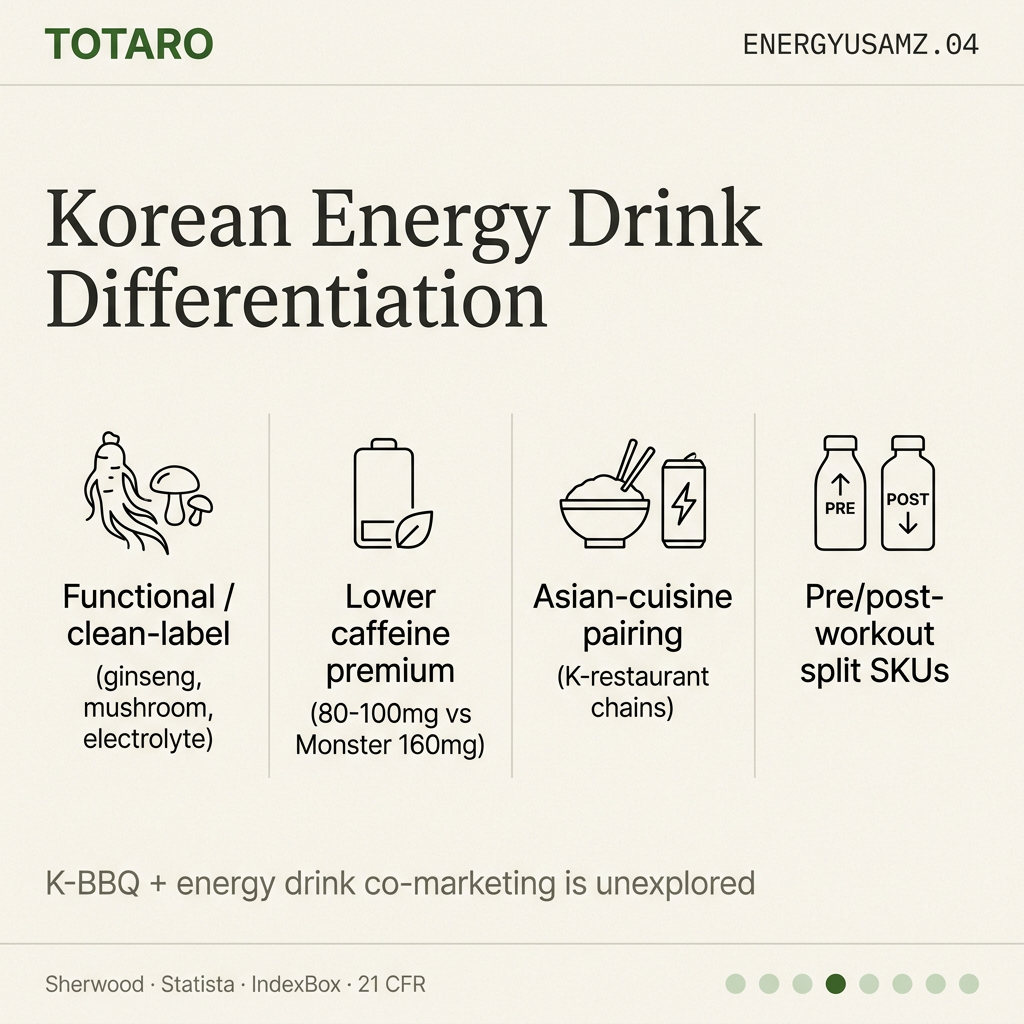

(1) Functional/clean-label angle — Korean ginseng energy, mushroom-extract energy, electrolyte + zinc + B-complex. (2) Lower caffeine premium — 80-100mg vs Monster's 160mg appeals to mid-day users. (3) Asian-cuisine pairing — bibimbap, Korean BBQ co-marketing in K-restaurant chains. (4) Pre-workout / post-workout split SKUs.

3. Channel Stack — Where to Start

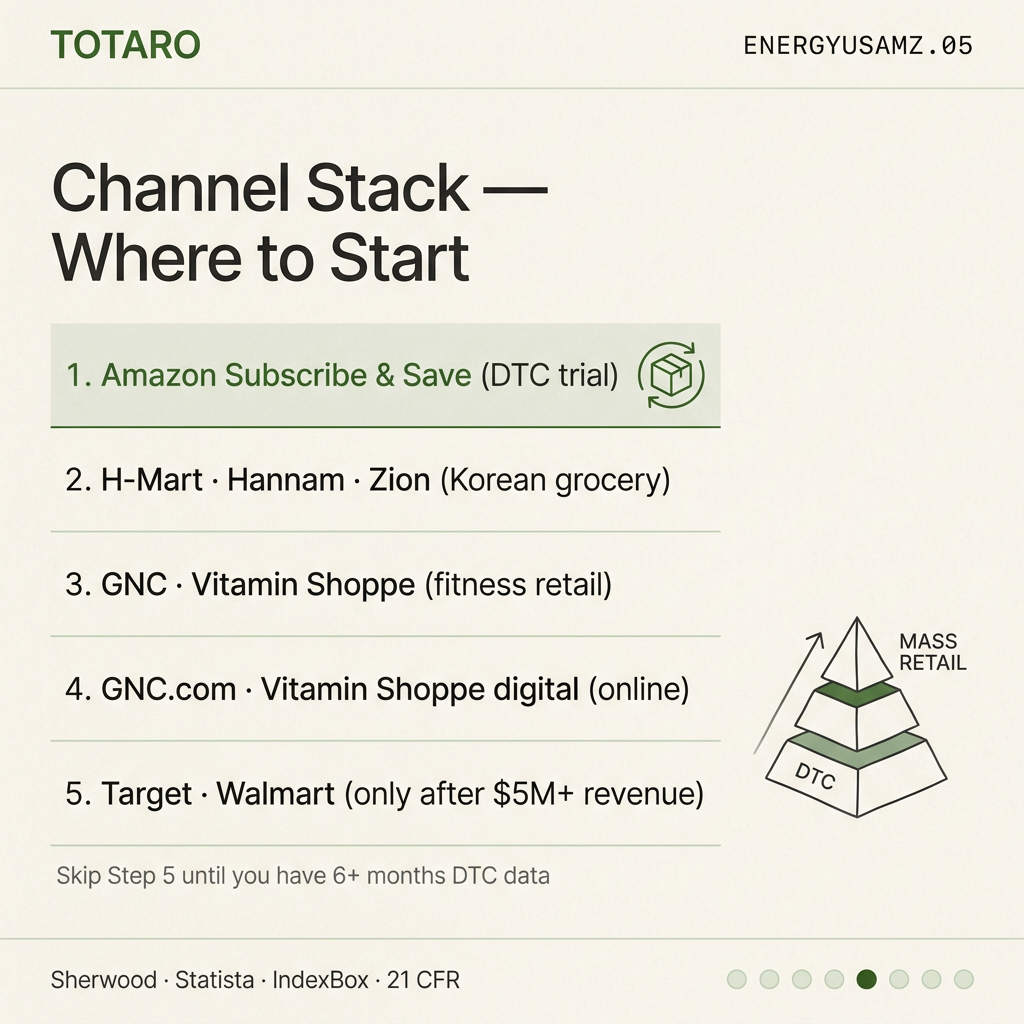

(1) Amazon Subscribe & Save — DTC trial channel. (2) H-Mart, Hannam, Zion — Korean grocery diaspora. (3) GNC, Vitamin Shoppe — fitness retail entry. (4) Vitamin Shoppe digital + GNC.com — online expansion. (5) Mass channel (Target, Walmart) — only after $5M+ revenue and 6+ months DTC data.

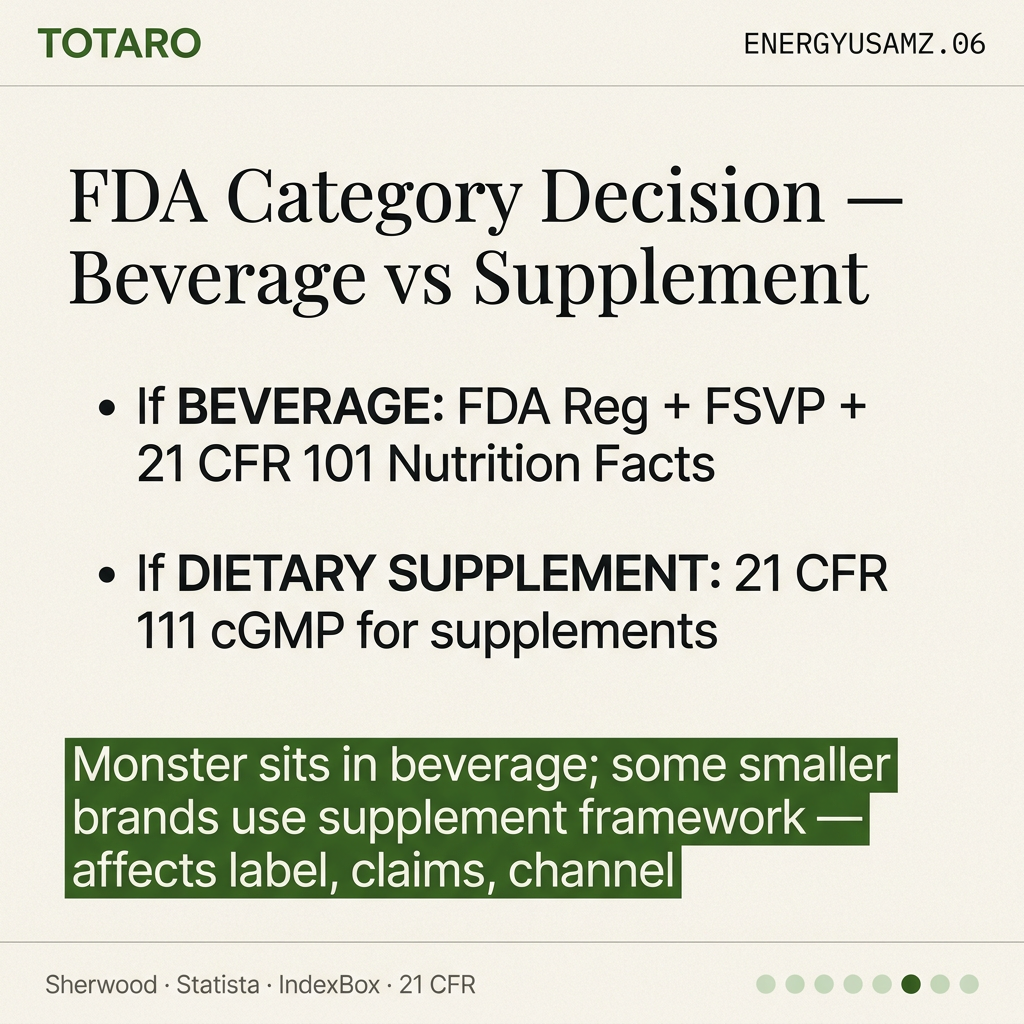

4. FDA Compliance for Energy Drinks

If marketed as beverage: FDA Foreign Facility Registration + FSVP + 21 CFR 101 Nutrition Facts. If marketed as dietary supplement: 21 CFR 111 cGMP for supplements (21 CFR 111). The category decision matters — Monster sits in beverage; some smaller brands use supplement framework. Caffeine content disclosure not mandatory but US energy buyers expect it.

5. Pricing Reality (MOQ / FOB)

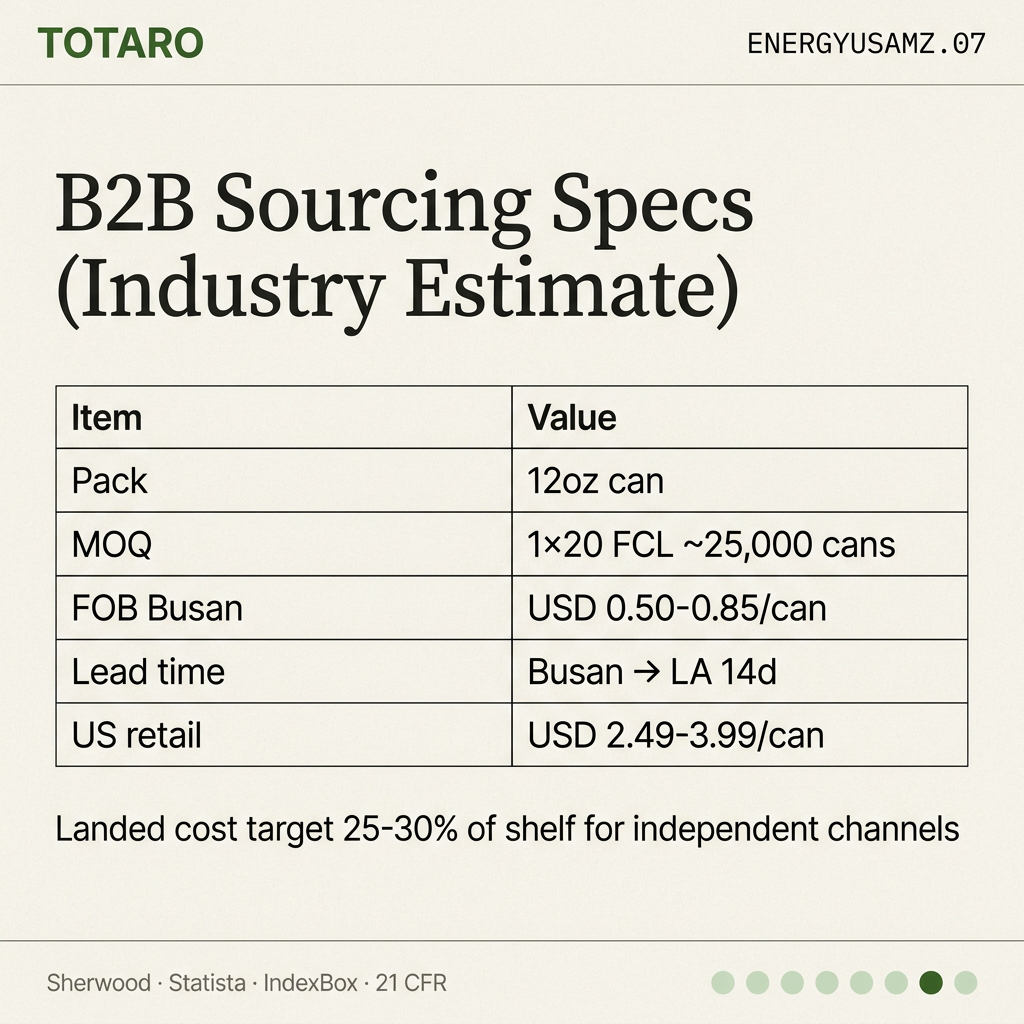

Industry estimate for 12oz can: MOQ 1×20' FCL (~25,000 cans), FOB Busan→USWC USD 0.50-0.85/can (early 2026). Direct RFQ required. US retail USD 2.49-3.99 per can; landed cost target 25-30% of shelf for healthy margin in independent channels.

6. Big 9 Allergen Considerations

Energy drinks rarely trigger Big 9 allergens unless milk or soy-protein included. Sesame (added Jan 2023) usually not applicable. Caffeine source (synthetic vs natural from green tea) affects label and consumer perception.

What to Do This Week

(1) Pick one differentiation angle (clean-label / functional / Asian-pairing). (2) Build Amazon Subscribe & Save listing with 4 unique value props. (3) Pitch to 1 fitness retailer (Vitamin Shoppe regional buyer). (4) Hold off on mass channel pitch until 6 months of DTC data. The Korean energy opportunity is open but only outside Monster/Red Bull territory.

Sources

Related Guides

Korean Jerusalem Artichoke + Psyllium Husk Halal Enzyme Supplement for the US: The SlimFox-Style Constipation + Weight Management Combo (2026)

Related Guides →Korean Jerusalem Artichoke for Constipation: 14-19% Inulin Content and Clinical Evidence on Gut Health (2026)

Related Guides →How to Import Korean Food into the USA: Complete 2026 Guide

Related Guides →Ask AI to find your Korean food supplier

Describe what you need in plain language — get matched with verified suppliers in seconds.

Try AI Supplier Search