카드 1 / 8

Korean Collagen and Inner Beauty for the US Market: Sephora's Pull-Back and the Olive Young Opening (2026)

TL;DR

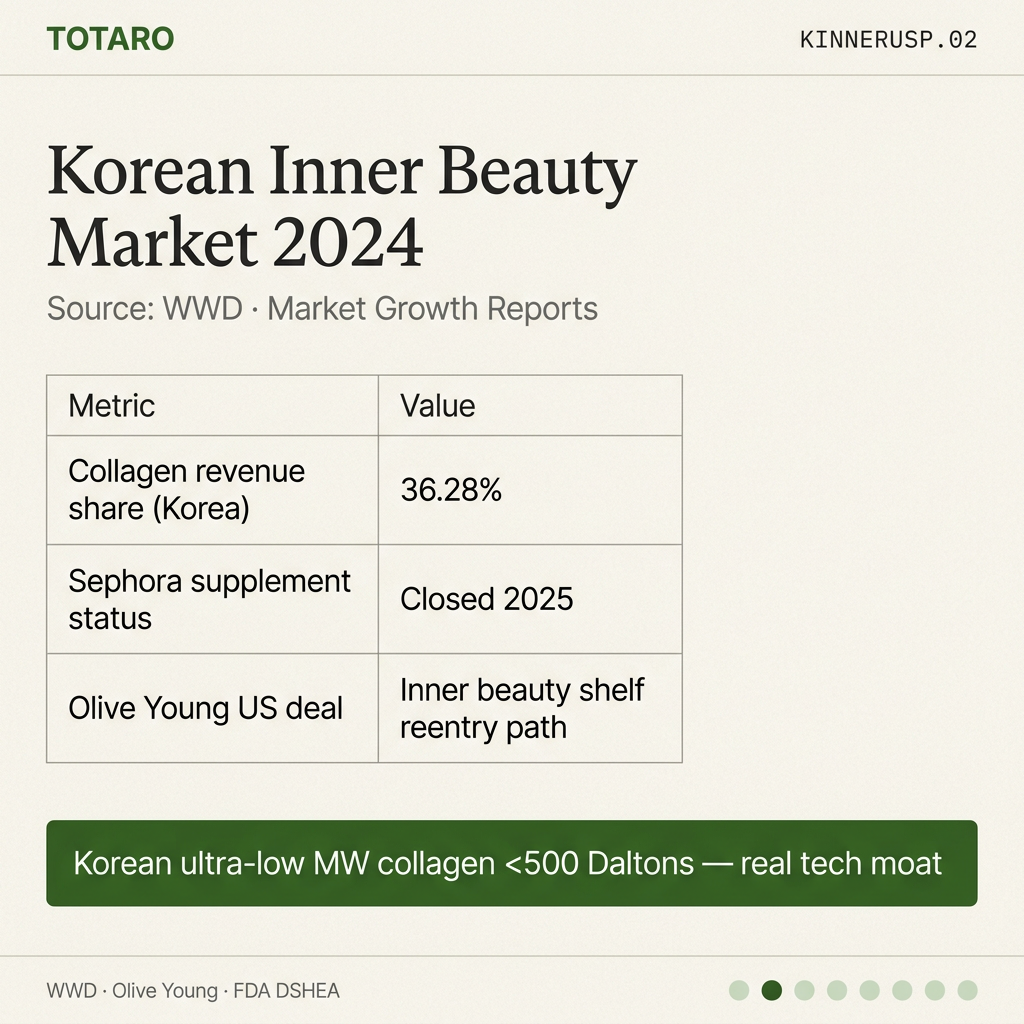

Collagen held a 36.28% revenue share of the South Korean skin supplement market in 2024 — the dominant inner beauty category. Sephora shuttered its supplement business in 2025 but inked a partnership with Olive Young that opens a potential reentry channel for Korean ingestibles (WWD — Korean Wellness). Korean collagen and inner beauty exporters should map their entry around this opening, not the closed Sephora supplement door.

1. The Market Structure

US inner beauty market is fragmented: Vital Proteins, Olly, Hum Nutrition dominate by channel (Target, Whole Foods, Amazon). Korean inner beauty enters through a different positioning: K-beauty extension (skincare brand authority transferred to ingestible) and functional clean-label (low molecular weight, no synthetic additives, traditional Korean botanicals).

2. Ultra-Low Molecular Weight — The Korean Tech Advantage

Korean collagen has shifted from general hydrolyzed collagen to ultra-low molecular weight under 300–500 Daltons for superior absorption — a real technical differentiator over US peers that mostly run at 2,000–5,000 Daltons. This is what US buyers (Sephora supplement category buyer, when they reopen; Whole Foods supplement; Amazon premium) want to hear.

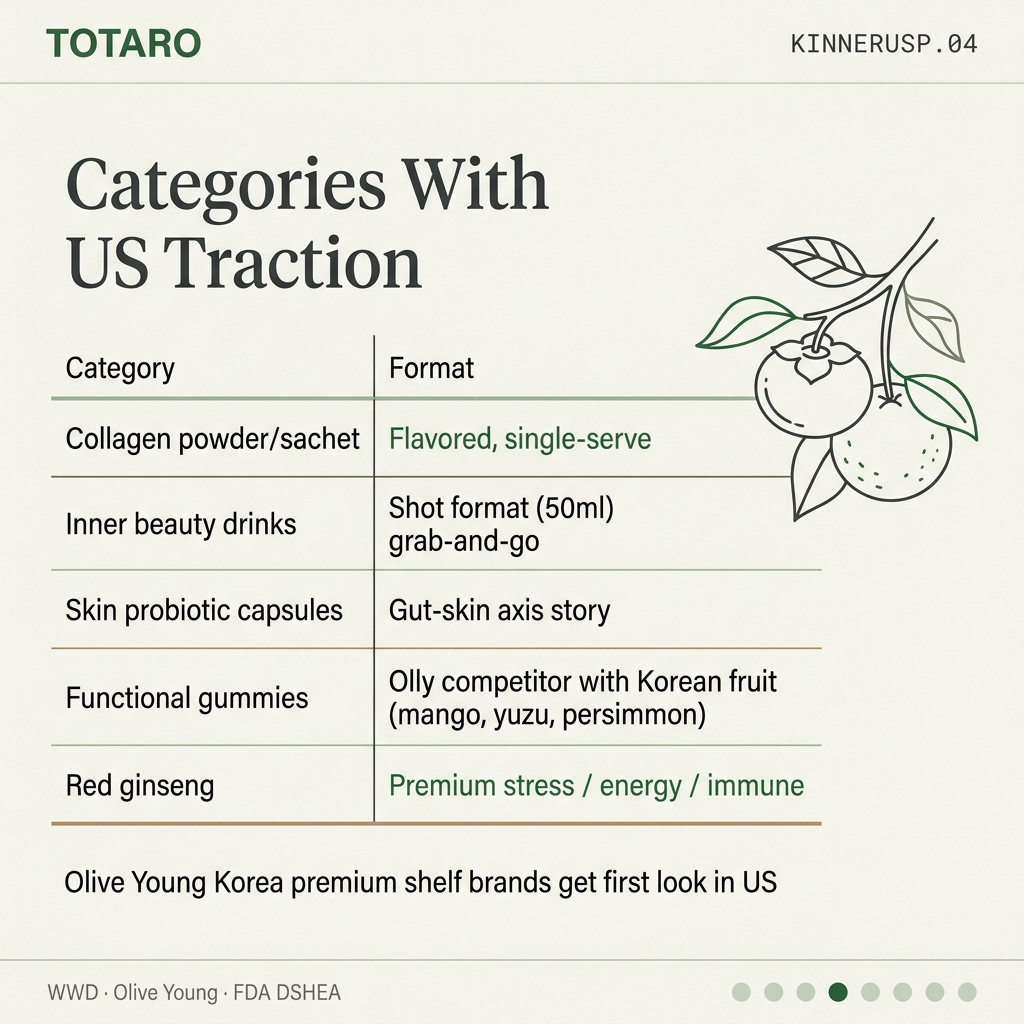

3. Categories With Highest US Traction

(1) Collagen powder/sachet — flavored, single-serve. (2) Inner beauty drinks — shot format (50ml), grab-and-go. (3) Skin probiotic capsules — gut-skin axis story. (4) Functional gummies — Olly competitor with Korean fruit (mango, yuzu, persimmon). (5) Red ginseng — premium positioning for stress / energy / immune.

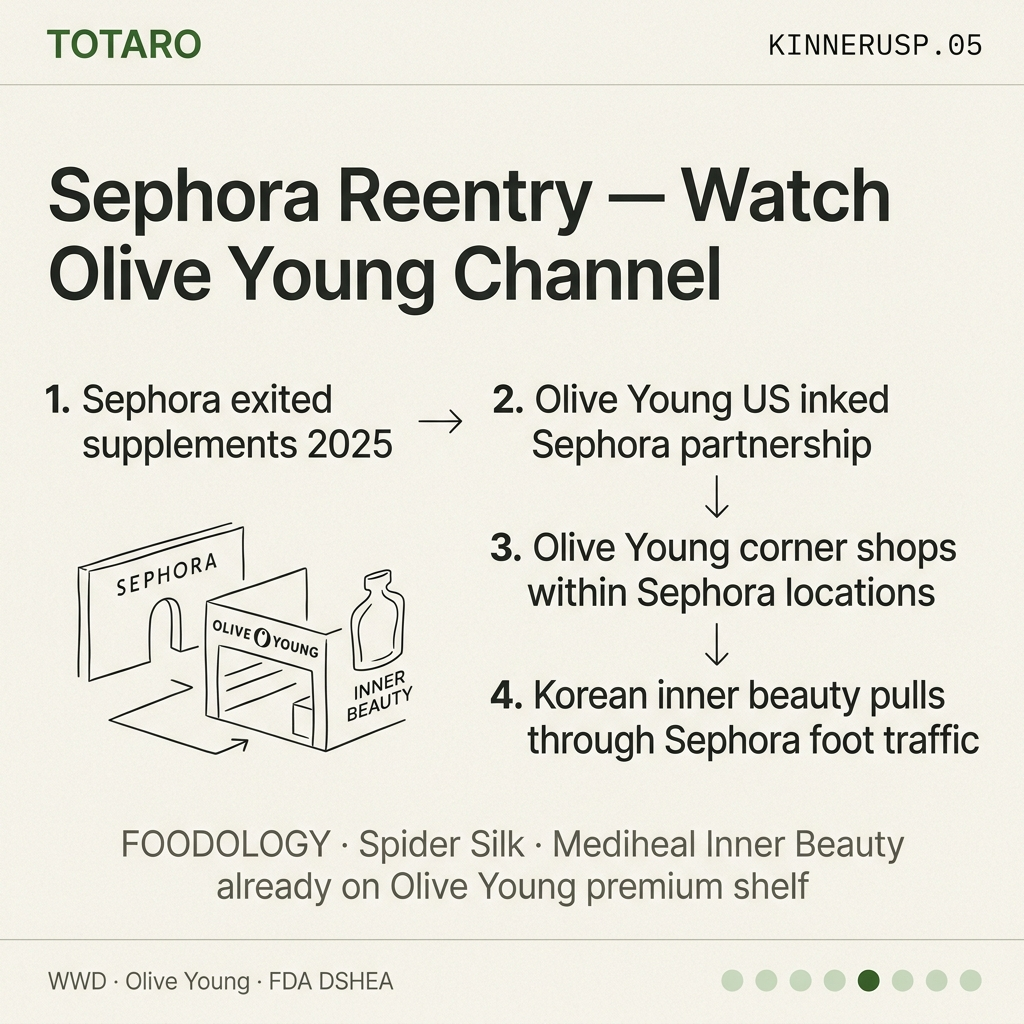

4. Sephora Reentry — Watch the Olive Young Channel

Sephora exited supplements but the Olive Young partnership is a strategic opening. Olive Young US opens corner shops within Sephora locations; the inner beauty SKUs from Olive Young's Korean lineup could pull through Sephora foot traffic. Korean inner beauty brands already on Olive Young Korea's premium shelf (FOODOLOGY, Spider Silk, Mediheal Inner Beauty) get a first-look.

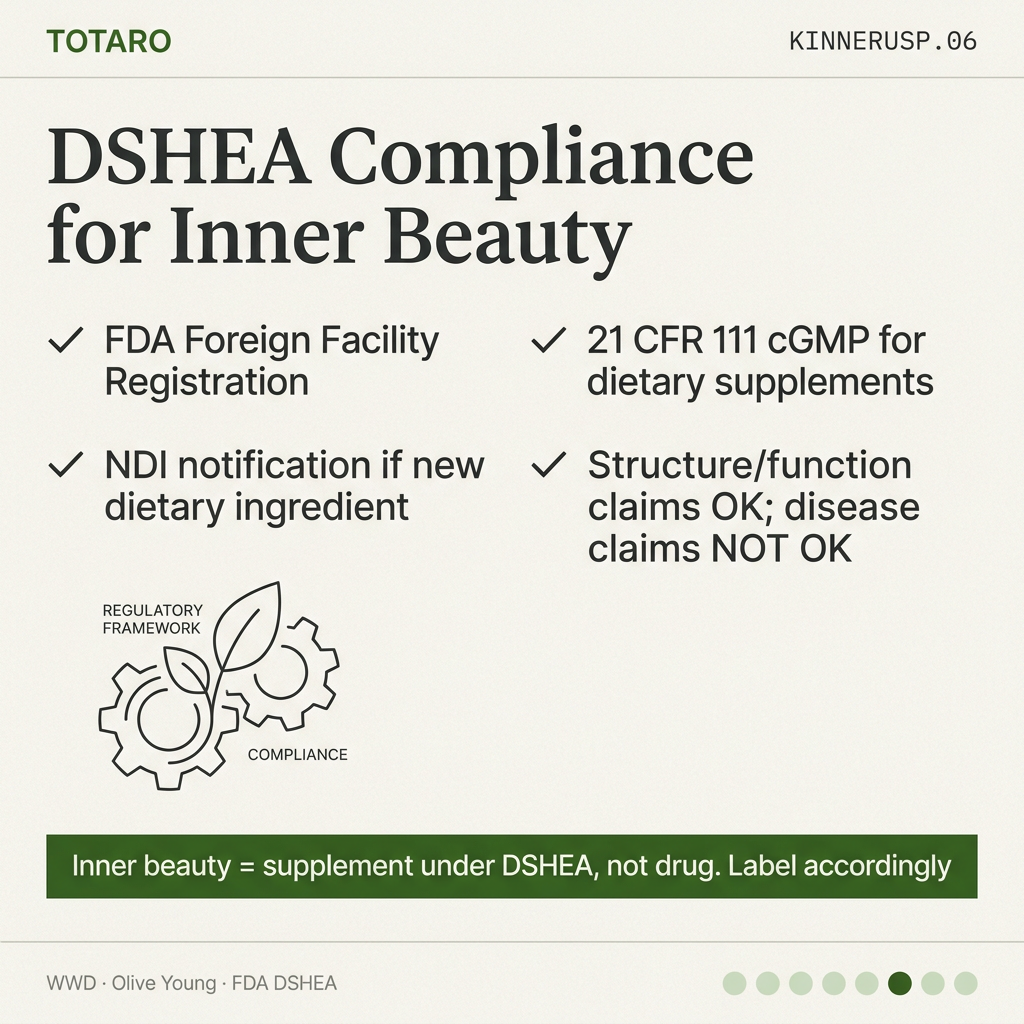

5. FDA Compliance for Inner Beauty Supplements

DSHEA framework applies — these are dietary supplements, not drugs. FDA Foreign Facility Registration (FDA), 21 CFR 111 cGMP for dietary supplements (21 CFR 111), NDI notifications if a new dietary ingredient is used (FDA NDI). Structure/function claims are allowed; disease claims are not.

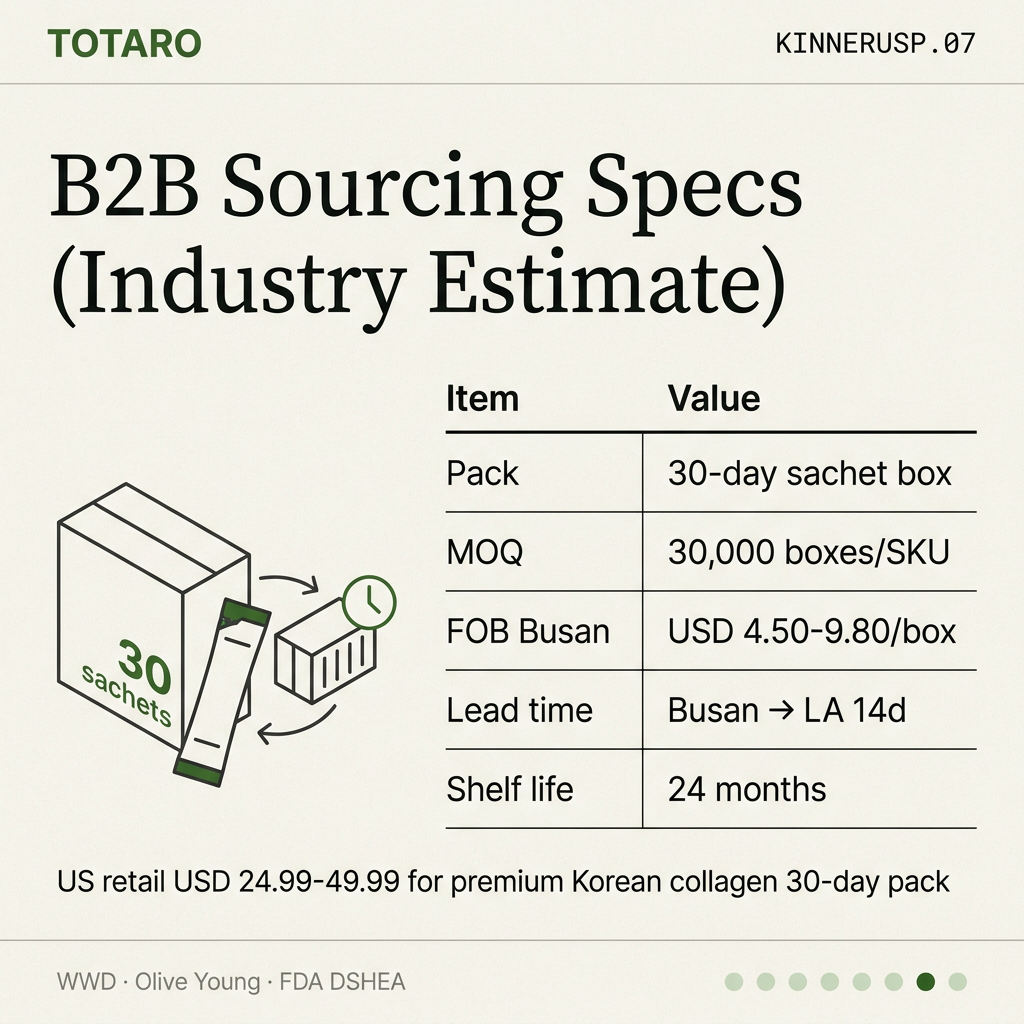

6. Pricing Reality (MOQ / FOB)

Industry estimate for inner beauty sachet 30-day box: MOQ 30,000 boxes per SKU, FOB Busan→USWC USD 4.50–9.80 per box (premium ingredient mix, 2026 early). Direct RFQ required. US retail USD 24.99–49.99 for premium Korean collagen 30-day pack.

What to Do This Week

(1) Pitch your story to Olive Young US merchandising — they're the gateway, not Sephora directly. (2) Apply to Amazon Premium Beauty for the supplement crossover. (3) Match your label to DSHEA structure/function claim language. The Korean inner beauty opportunity in the US is real and growing — Sephora's exit just rerouted it through Olive Young.

Sources

Related Guides

Korean Jerusalem Artichoke + Psyllium Husk Halal Enzyme Supplement for the US: The SlimFox-Style Constipation + Weight Management Combo (2026)

Related Guides →Korean Jerusalem Artichoke for Constipation: 14-19% Inulin Content and Clinical Evidence on Gut Health (2026)

Related Guides →How to Import Korean Food into the USA: Complete 2026 Guide

Related Guides →Ask AI to find your Korean food supplier

Describe what you need in plain language — get matched with verified suppliers in seconds.

Try AI Supplier Search